In a newspaper advertisement last Monday, Tata Capital said that it has filed its draft red herring prospectus with the Securities and Exchange Board of India (Sebi) to float its maiden public issue. The filing was made through the confidential route in which no details of the proposed issue are disclosed to the public.

Reports in newspapers suggested the public offer of shares could be worth ₹15,000– ₹18,000 crore, making it one of the largest in the financial services industry and only the third IPO of any Tata company in the last 25 years. The two others are Tata Consultancy Services in 2003 and Tata Technologies in 2023.

Right away, the timing to list appears to be in response to a central bank stipulation in September 2022 that needed companies like Tata Capital to list on stock exchanges. Based on the scale of operations, the central bank had classified non-bank finance companies on different levels and made listing of the large and systemically important ones mandatory within three years or September 2025. Tata Capital was classified as an upper-layer finance company, requiring it to be listed within that time frame.

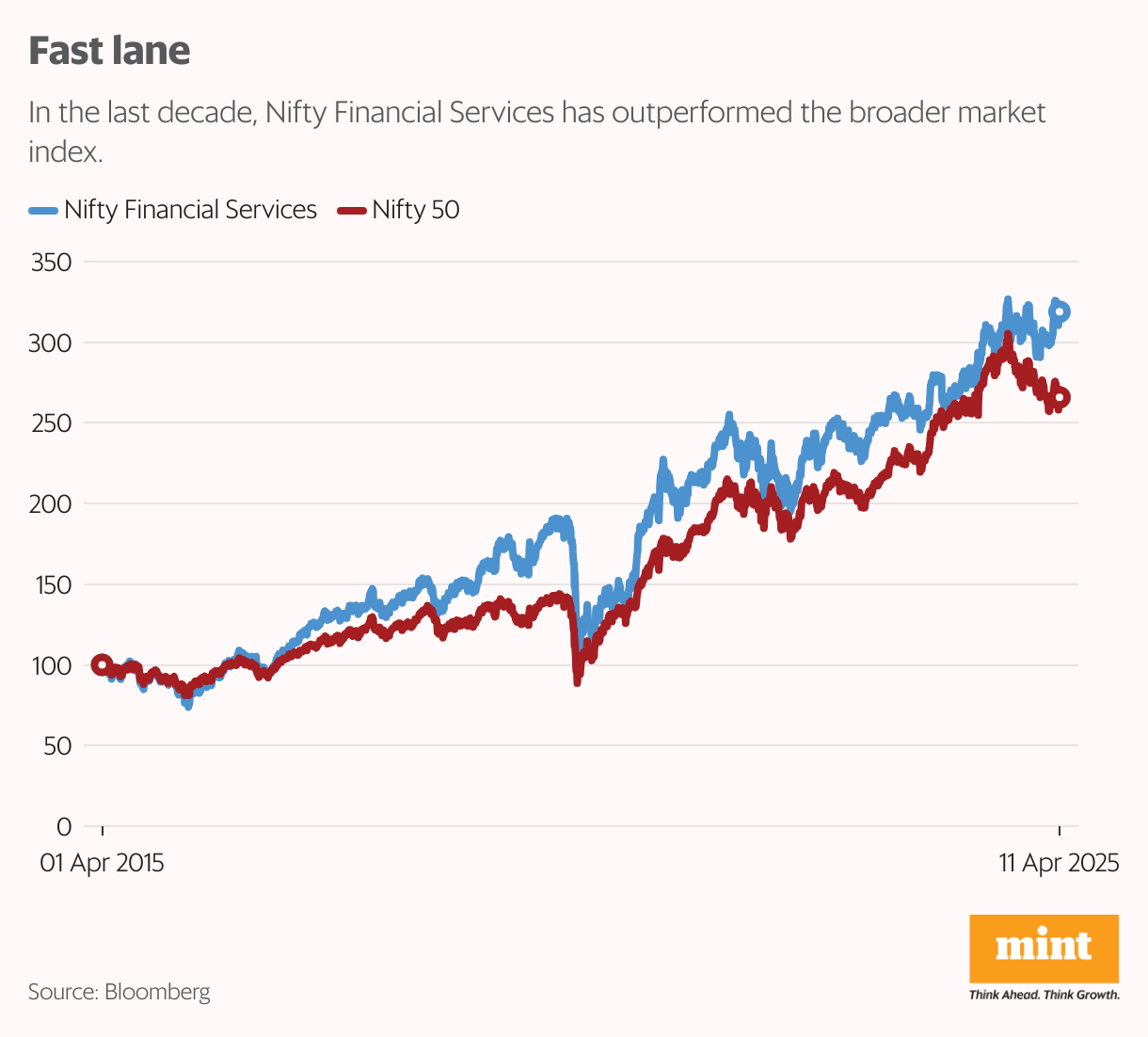

For equity investors and the stock market, the Tata move may appear to have come a little late in the day. Banking and financial services companies account for a fifth of Nifty 50 companies and 26% of its market capitalization. Seven out of the top 20 most valued companies in the Nifty are either banks or financial services companies. Tata contemporaries—other large business houses like the Aditya Birla group, Reliance, Mahindra’s or the south-based Murugappa group—have all taken the lead and listed their finance companies and benefited from the valuation growth in the sector in recent years.

The late move is also marked with a bit of irony. Historically, the Tata group was one of the earliest to have had an interest in banking and financial services—the nationalized Central Bank of India had its roots in Tata Bank while New Indian Assurance, started in 1919, was owned by the group. Subsequently, when foreign capital was allowed in the domestic insurance business, Tata invested in two insurance joint ventures in the ’90s and operated two non-banking finance businesses including a listed entity until 2003.

Says Ajay Garg, managing director of investment banking firm Equirus Capital: “The addition of Tatas to the roster of financial sector firms in the country is a big event. You can expect them to set benchmarks in corporate governance in the industry but it remains to be seen if they can innovate enough to stand out in the hyper-competitive industsry.”

The Tata group did not respond to clarifications sought by Mint.

Always in focus

To be sure, finance was always a key area of business and investment for the group though Tata Capital flew under the radar for two reasons—the company did not grow as fast as its competitors and being unlisted, there weren’t many disclosures it needed to make to regulatory authorities.

The group’s first non-banking company, Tata Finance, was incorporated in 1984 and subsequently listed. It aimed to be a full-fledged financial services company with merchant banking and broking licenses. Investors highly sought after its fixed deposits as it was a rare firm that emerged from a mid-90s meltdown in non-banking financial services businesses that took down several firms like the Arvind-owned Anagram and the Cipla-owned Alpic. Tata Finance was itself dissolved and merged into Tata Motors in 2003 after a subsidiary company’s investments in stock markets wiped out its capital. In effect, this is the second attempt of the Tatas to build the business.

After a brief hiatus, the current iteration of the financial services business started in 2007, just before the Lehman-induced global financial crisis rocked the markets. Tata Capital would become the new vehicle of the group’s ambitions in finance and it deputed Praveen Kadle, till then the chief finance officer of Tata Motors, to head the business. Kadle was instrumental in putting right the automaker’s finances post its massive loss of ₹500 crore in FY01 and resolving the problems created in Tata Finance.

")

View Full Image

It was not the best of beginnings. The financial services business required capital but the Tata group was in a debt crisis as it required huge amounts of cash to pay for its acquisitions of UK-based Jaguar Land Rover and steel company Corus Plc. In its early years, Tata Capital extended loans to several infrastructure companies that went bad. In his letter to the directors of Tata Sons in October 2016, ousted chairman Cyrus Mistry wrote: “Tata Capital had a book that required significant clean up on account of bad loans to the infrastructure sector. All of this resulted in Tata Capital having to recognize the abnormal size of NPAs (non-performing assets).”

Says Nirmalaya Kumar, Lee Kong Chian professor of marketing in Singapore and ex-confidante of Mistry: “In our Strategy 2025 document that was prepared in 2015, we had envisioned the finance business to be one of the most important growth areas for the Tata group for the next decade. Its importance was ahead of even the consumer business where the group had begun investing heavily.”

The immediate fallout of lack of capital was that Tata Capital never expanded its portfolio in the more profitable retail lending business, which was seeing a big spike after the biggest player in the business, ICICI Bank, reduced its exposure to unsecured loans. A big chunk of its customers was from the extended Tata ecosystem of dealers and associates, according to a Crisil rating report.

“In 2015, the Tata group was staring at several impairments in its telecom business. Nobody then paid much attention to the financial services business which is known to be a cash guzzler. Given the issues with the core businesses, retail lending was not even under consideration,” Kumar says.

In its early years, Tata Capital extended loans to several infrastructure companies that went bad. In his letter to directors of Tata Sons in October 2016, ousted chairman Cyrus Mistry wrote: “…this resulted in Tata Capital having to recognize abnormal size of NPAs.”

All this meant Tata Capital’s business growth lagged behind as compared to its competitors. In FY17, Bajaj Finance had assets worth ₹42,755 crore and posted net profits of ₹12,644 crore while Tata Capital’s consolidated assets stood at ₹37,269 crore and profits at ₹1,247 crore.

There were also other tricky issues that needed to be resolved. In the legal battle between Mistry and Ratan Tata, who took over the helm of the group again, a ₹200 crore loan given by Tata Capital to Siva Industries became a contentious issue. Siva Industries defaulted on the loan and its promoter C. Sivasankaran was considered a close ally of Tata. Until his sudden ouster from the board, Mistry neither wrote off the loan nor did he give additional capital to Tata Capital which ended up stymying its growth.

A makeover

The fortunes of Tata Capital slowly began to change after Mistry’s successor, N. Chandrasekaran, took over as group chairman in February 2017.

In July 2017, Chandrasekaran hired Saurabh Agarwal, an investment banker and the head of strategy at rival Aditya Birla group as Tata Son’s chief financial officer. Under Agarwal’s watch, the Birla group had listed their finance arm and expanded into several retail businesses like lending and wealth management. Agarwal joined the board of directors at Tata Capital and in doing so, Chandrasekaran may well have scripted a new game plan for the group’s financial services ambition.

Incidentally, Kadle was retiring in March 2018 and that gave the new management space to think afresh about their goals. Tata Capital picked an ex-ICICI Bank senior executive, Rajiv Sabharwal, to helm the company. “Our brief was simple: grow twice as fast as the industry and build a credible retail franchise,” a former Tata Capital executive, who didn’t want to be identified, says.

The business portfolio also needed an overhaul. Under Kadle, Tata Capital did wholesale, corporate lending and rural lending.

Sabharwal’s brief, however, was to steer Tata Capital away from high volume, low margin wholesale and corporate finance to the fast-growing retail space and to lend more unsecured loans to increase profitability. With returns proportional to risk, unsecured loans attracted more interest than corporate loans leading to better profitability. The strategy was a no-brainer.

Critically, money also started flowing into the company quickly. In July 2018, Tata Sons wrote a cheque of ₹1,250 crore and one more of a similar amount in March 2019. A Crisil rating note, appraising a subsidiary company’s bank loan facility, said that it drew confidence from the fact that Tata Sons was bringing in as much capital in FY19 as it did since its inception. Tata Sons had infused ₹2,800 crore in Tata Capital from 2007-18.

The clean-up started with business lines like infrastructure and agri loans being shut while new lines like housing finance and loans to clean tech were made focus areas.

“It was not an easy path as there were already several established players in the retail space. Within housing finance, we focused on loans for buying low-cost homes as it came with lower delinquencies. We got it wrong a couple of times but we will now rank among the top three in the space,” Tata Capital’s former executive, quoted above, says.

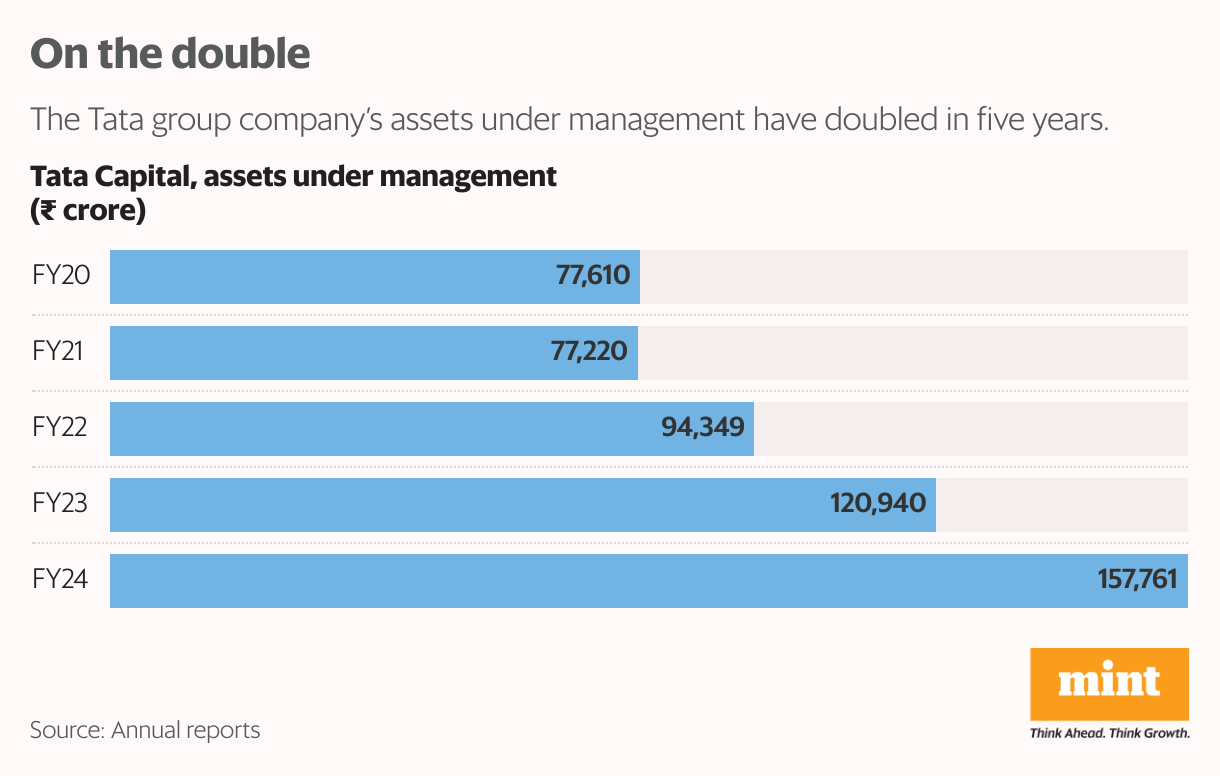

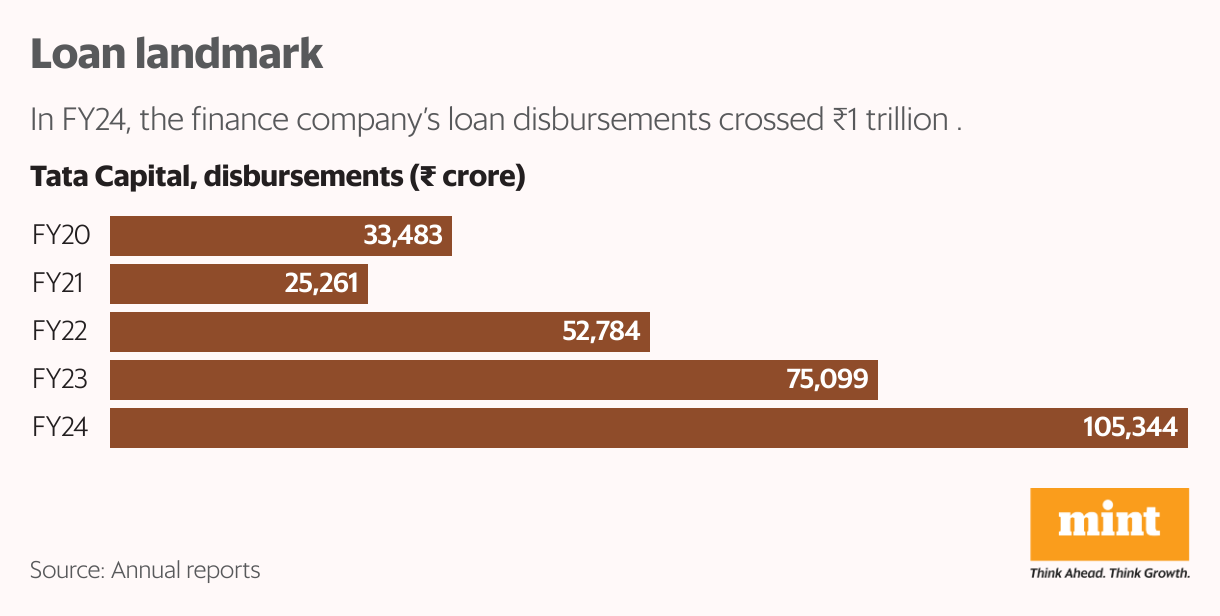

In FY24, the company’s loan disbursements crossed ₹1 trillion annually and retail and SME constituted 85% of its ₹1.5 trillion book. Though it also distributes mutual funds, it hasn’t been able to grow this business as the company hasn’t been able to make much headway in digital sales.

As a prelude to its listing, Tata Motor Finance, a wholly owned subsidiary of Tata Motors, has been merged with Tata Capital. This has been done to put all the finance businesses of the company under one entity. Incidentally, the legacy of Tata Motor Finance began with the merger of Tata Finance into Tata Motors in 2003.

As of FY24, Tata Motor Finance’s accumulated losses to be carried forward totalled ₹1,135 crore. It will now be transferred to Tata Capital. Since the merger was effective in the current financial year, the draft prospectus is likely to contain details of any impairment.

One of many

When the Tatas began their financial services business in the 80s, it was among the early birds in the sector dominated by mostly unregulated chit-fund companies and public sector banks. But today it faces big competition from not just established private sector finance firms like Bajaj Finance and Murugappa group’s Cholamandalam Finance but also from private sector banks like HDFC Bank and ICICI Bank, which use their wide distribution to push for retail loans. Besides, the playfield today has a swathe of fintech startups that can upend micro markets through faster access to credit.

Says Garg: “Banks have an inherent advantage with their low cost of funds from retail deposits and therefore they will set profitability benchmarks that Tata will have to beat.”

On its part, Tata Capital has sought to keep itself as different from the pack as possible. In its annual report, the company says that it is one of the top-three diversified financial services firms in the country and 92% of its over 700 branch offices are in non-metros. And that 83% of its 4.5 million customers in FY24 are from non-metros, too.

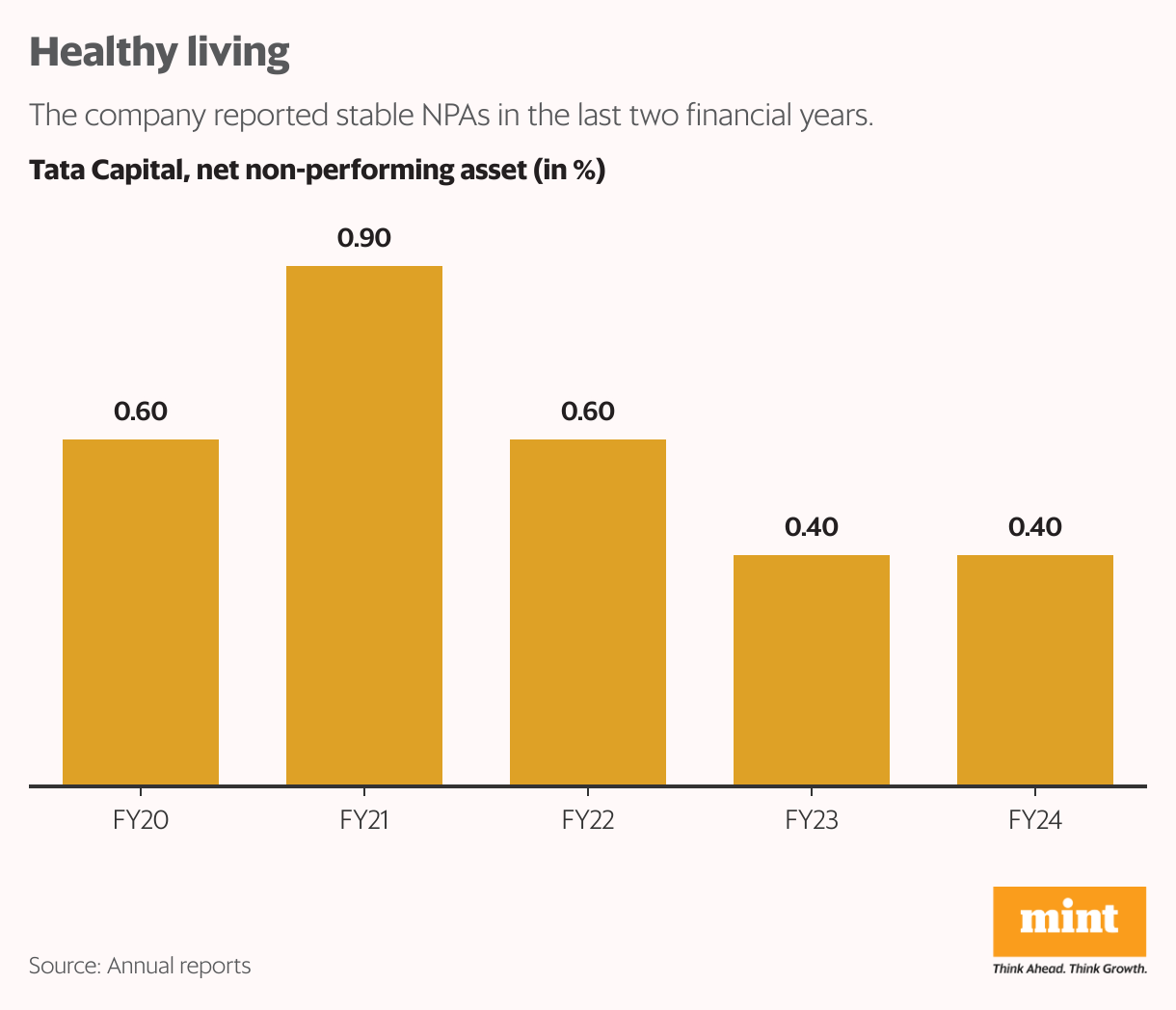

Tata Capital also oversees five private equity funds in its portfolio— four domestic and one overseas fund that have investments spread across sectors like healthcare and capital innovations. Its net non-performing assets in the year at 0.4% is better than large competitors like Cholamandalam Finance and LIC Housing Finance.

The company has added microfinance to its portfolio during the year, spreading its arm in almost every important gamut of financing in the country. Says a senior board member of a Tata group company who didn’t want to be identified: “Large conglomerates like Tata, Aditya Birla and Reliance want banking licences and perhaps, that idea still lingers on even though the RBI has paid put to those thoughts, at least for now.”

Meanwhile, Tata Capital going public could bring heft to the non-banking sector. It is common knowledge that RBI meted out a step motherly treatment to the sector for its lack of systems and processes. The arrival of a Tata company in the scene is expected to change that.

“If the Tatas call upon the RBI, they will certainly get a hearing. That in itself will be a big change for the sector as a whole,” a retired deputy governor from the central bank says. He didn’t want to be identified.

Leave a Reply